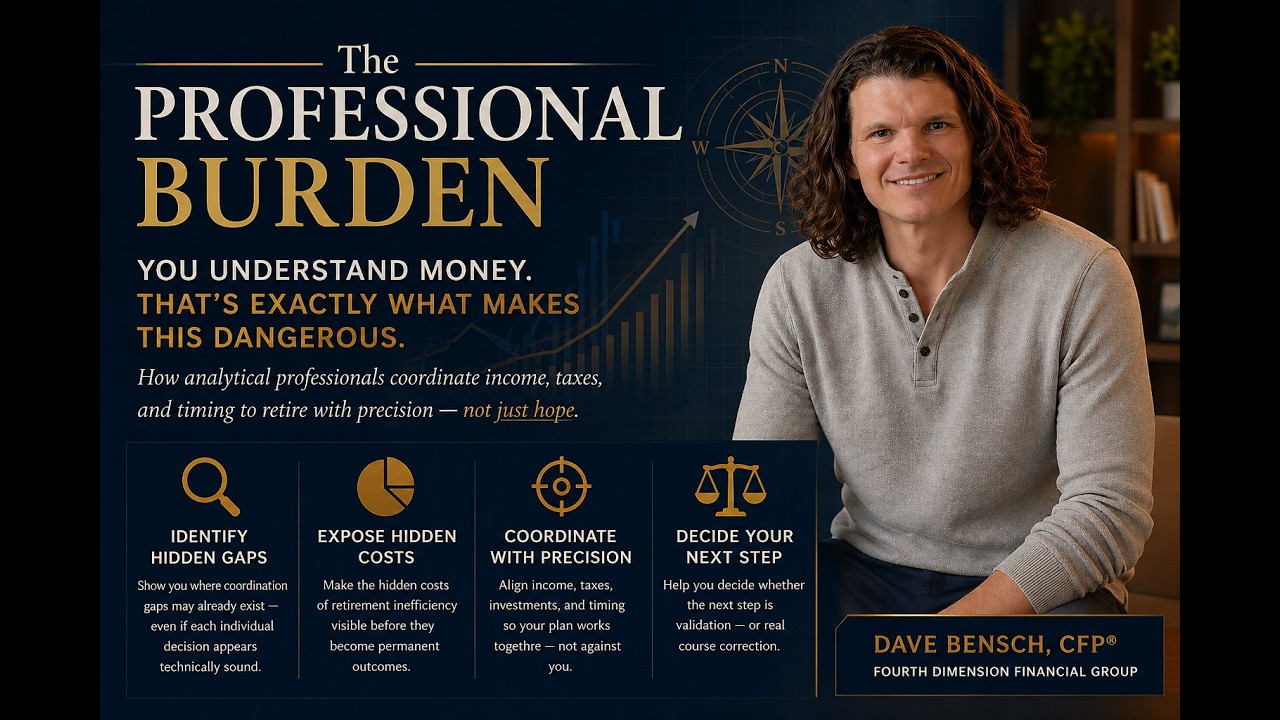

You Understand Money.

That's Exactly What Makes

This Dangerous.

How analytical professionals coordinate income, taxes, and timing to retire with precision — not just hope.

The Retirement Red Zone Changes the Rules Completely

There is a period in your financial life where the decisions you make — individually reasonable, technically defensible — can combine to produce a retirement that is significantly less efficient than it should be.

The people most likely to miss retirement inefficiencies are the ones smart enough to feel confident they haven't. It's not a knowledge problem. It's a coordination problem.

| During Accumulation | During the Red Zone |

|---|---|

| Time absorbs most mistakes | Mistakes compound forward with no real recovery window |

| Tax decisions are relatively siloed | Tax decisions interact across multiple income streams and decades |

| Investment allocation is the primary lever | Withdrawal sequence, Social Security timing, and tax structure become equal levers |

| Errors are correctable | Many decisions are permanent or very costly to reverse |

Most retirement inefficiencies don't announce themselves. They show up years later as higher-than-necessary taxes, lower-than-possible income, and less flexibility at exactly the moment you need it most.

Analytically capable professionals often arrive at retirement with detailed spreadsheet models of their financial picture. They've run the numbers. They've stress-tested assumptions. They feel confident in the math.

What those models frequently don't capture is how multiple variables interact simultaneously in distribution — specifically, how a significant market decline early in retirement, combined with ongoing withdrawals, can permanently impair a portfolio's ability to recover. This isn't a modeling error. It's a structural difference between accumulation and distribution that single-variable analysis doesn't surface.

Analytically capable people tend to model accumulation well. Distribution is structurally different — the variables interact across time in ways that sequential spreadsheet modeling doesn't fully capture.

Sequence of returns risk, in particular, rewards preparation rather than reaction. By the time the pattern becomes visible, the options to respond have already narrowed significantly.

Dave stress-tests retirement plans against multiple scenarios — including significant early-retirement market declines — to identify which income sources need to be sequenced to protect the long-term portfolio from forced liquidation during a downturn.

The goal isn't a more conservative plan. It's a more resilient one — built to hold across conditions that can't be fully predicted, while preserving flexibility when it's needed most.

How Coordinated Is Your Retirement Strategy, Really?

Yes

Yes

Yes

Start answering the questions. As you do, your result will update here automatically.

If you do not confidently answer "yes" to every question, that is exactly where this process begins. The goal is not to prove anything. The goal is to identify what still needs to be coordinated — while you still have time to act on it.

Most analytical professionals can model each retirement variable in isolation. The coordination problem happens when all of those variables are pulled simultaneously across decades — and no single spreadsheet captures how they compound against each other.