The Blueprint for Responsible Retirees

How families who did everything right finally get the retirement they deserve — with a coordinated plan built around their life, not a generic template.

Take the free standalone Retirement Risk Score quiz

The Moment of Truth

You saved for thirty years. You made sacrifices. You stayed the course when the markets got scary. You did what you were supposed to do.

But here's what most people discover too late:

The decade surrounding retirement is the most financially dangerous period of your life.

Not because you made mistakes. Because no one helped you navigate what comes next.

The years just before and just after retirement — the Retirement Red Zone — are where the rules change completely. Income, taxes, Social Security, investment risk, and Medicare all collide at once. And the decisions you make during this window are largely permanent.

This is not about fear. It's about being prepared. And preparation starts with understanding the terrain ahead.

Many disciplined savers arrive at the edge of retirement with strong account balances and years of responsible financial habits behind them. On paper, everything looks solid. But when the conversation shifts from what has been saved to how those savings become reliable monthly income — the clarity starts to fade.

The assets exist. The income plan does not.

Most pre-retirees have accumulated assets but have never built a coordinated picture of how those assets become income — or what taxes, Social Security timing, and Medicare costs will do to that income once it starts. Each account has been managed. No one has mapped how they work together.

The pieces exist. The structure does not.

Dave starts by organizing the full picture — not just what has been saved, but how each piece is meant to work together. Income is mapped before retirement begins. Tax exposure is evaluated across years, not just annually. Social Security timing is analyzed as part of the integrated plan, not as a standalone decision.

The goal is simple: replace uncertainty with a clear, coordinated path forward.

The Retirement Red Zone

There is a financial truth that almost no one talks about clearly:

The five to ten years before and after retirement carry more risk — and more opportunity — than the previous three decades combined.

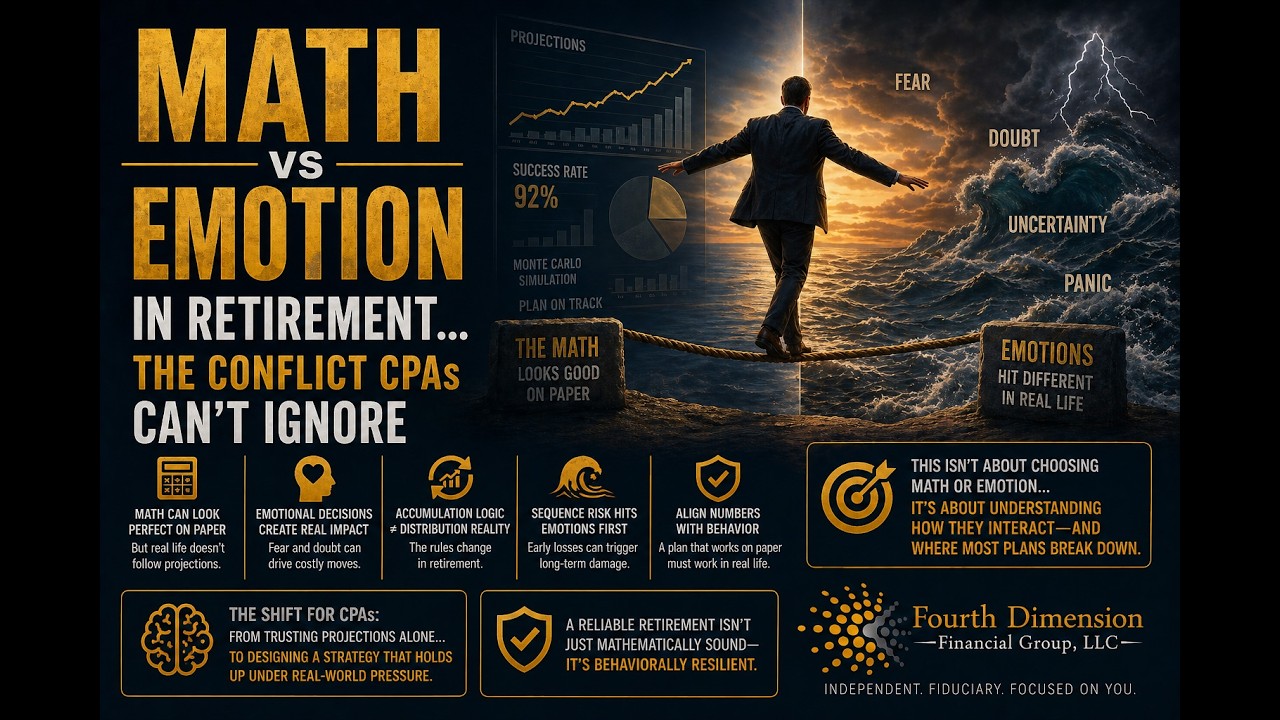

This isn't an opinion. It's math. A market drop at 45 is an inconvenience. A market drop at 67, when you're drawing income from your portfolio, can permanently alter what your money does for the rest of your life. The technical term is sequence of returns risk. The human term is: running out of money before you run out of life.

But market timing is only one part of the story. Layered on top of it are decisions that most people make without fully understanding the consequences:

- When you claim Social Security — and how that decision compounds across 20+ years

- How you withdraw from your accounts — and how the wrong order quietly inflates your tax bill for decades

- When you convert to Roth — and the narrow window that makes this most powerful

- How your investments are structured — and whether they're built for accumulation or distribution

- How Medicare costs shift based on income — and how a single uninformed decision can cost thousands per year

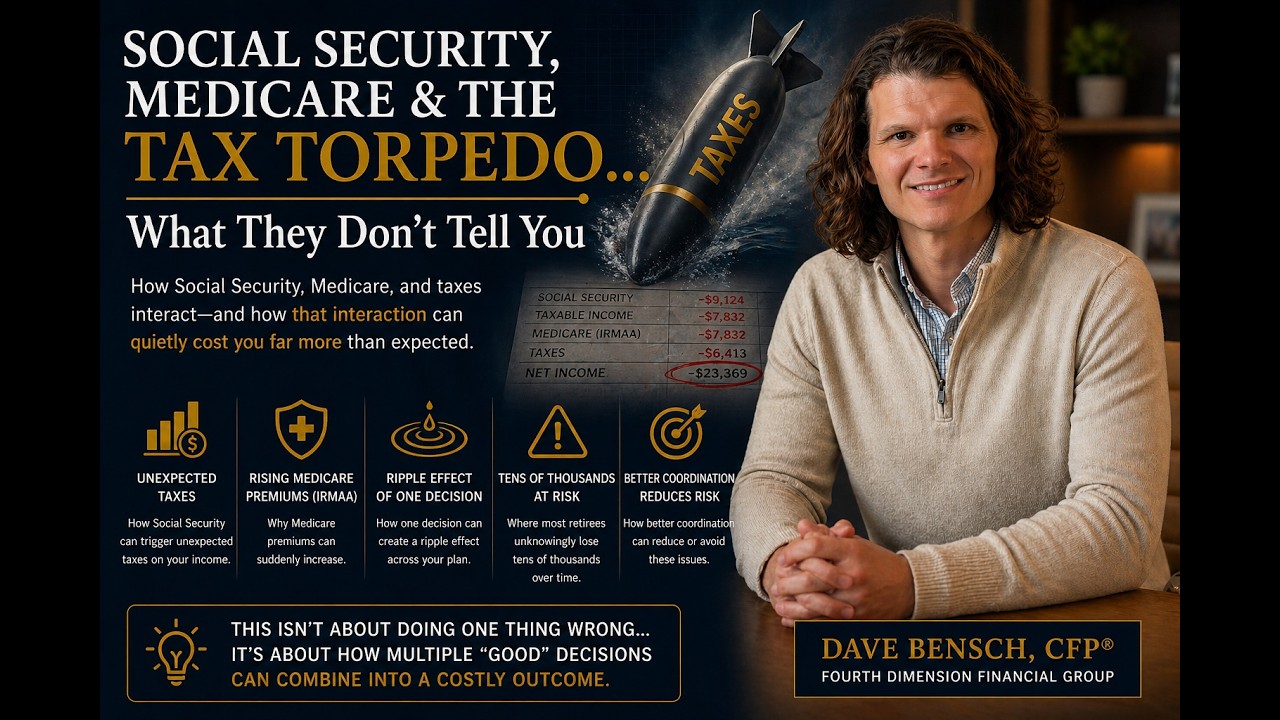

Many retirees who did everything right during accumulation find themselves facing a growing tax burden in retirement — not because their income increased, but because multiple income sources began interacting in ways no one had explained.

Required Minimum Distributions stack on top of Social Security. Social Security becomes partially taxable. Medicare premiums rise. Each piece seemed manageable in isolation. Together, they create a tax picture that looks nothing like what was expected.

No one had mentioned this was coming.

The collision of RMDs, Social Security taxation, and IRMAA Medicare surcharges — sometimes called the tax torpedo — catches many retirees off guard. Each element is understandable on its own. The interaction between them is not intuitive, and rarely gets modeled in advance.

By the time most people see it clearly, the window to restructure has already narrowed significantly.

Dave maps these interactions before retirement begins — before a single dollar is withdrawn. By modeling RMD projections, Social Security taxation thresholds, and IRMAA brackets together as a single coordinated picture, he identifies where the tax torpedo is likely to hit and builds a withdrawal sequence and Roth conversion strategy designed to reduce its impact.

The earlier this work begins, the more options remain available.

Is This You?

You are not someone who made reckless choices. You built this carefully, over a long time. You made sacrifices along the way. You took your savings seriously when others spent freely.

But now, as retirement gets close, the questions that used to feel distant are suddenly urgent:

These are not the questions of someone who failed. They are the questions of someone who is paying attention — someone who understands that getting this right matters. They deserve real answers. Not guesses. Not generic advice. Not a product pitch.

If you recognize yourself in those questions, this Blueprint was built for you.

Many people approaching retirement have been working with the same financial advisor for years — sometimes a decade or more. The annual reviews happen. The portfolio gets discussed. But the questions that actually keep people up at night — about Social Security timing, about what happens to a spouse financially if they go first, about whether taxes are being managed or just accepted — never seem to get addressed.

After a while, people stop bringing them up. They assume the advisor has it handled. Or that the answers are too complicated to get into.

When important questions go unanswered for long enough, people begin to assume they're being managed — that silence means everything is fine. What it more often means is that those questions fall outside what most investment-focused advisors are trained or structured to address.

Income planning, tax sequencing, Social Security coordination, and survivor protection require a different kind of conversation. Most advisory relationships are never built around one.

Dave's first conversations are built around questions, not presentations. Before any recommendation is made, he works to understand the full picture — what income will look like, what the tax exposure is, what Social Security timing means for both spouses, and what the surviving partner's financial situation actually looks like.

Most people leave that first conversation having had discussions they never had in years of working with someone else.

Where Good Plans Break Down

The people who struggle in retirement are rarely reckless. They're careful, thoughtful people who made decisions that seemed reasonable at the time — without understanding how those decisions ripple forward across twenty or thirty years.

They withdrew from the wrong accounts first and handed extra money to the IRS — not once, but every year for the next two decades. They claimed Social Security when it felt right, not when the math said to. They kept investing the way they always had, without realizing that the rules change completely when you're spending down instead of building up.

They left a surviving spouse with a tax burden no one warned them about. They paid Medicare premiums that could have been avoided. They never had a structured income plan, so every market drop felt like a crisis.

None of these are dramatic failures. They are quiet inefficiencies — decisions that feel fine in the moment and cost tens of thousands of dollars over time.

The problem is never that people made bad choices. The problem is that no one showed them what the right choices looked like — before it was too late to change course.

Many retirees enter distribution with a withdrawal strategy that feels completely logical — draw from the largest account first, keep things simple, adjust as needed. What isn't visible in that approach is how IRA withdrawals interact with Social Security taxation, Medicare premium thresholds, and the trajectory of future Required Minimum Distributions.

The plan feels fine. The tax consequences are compounding quietly in the background.

Withdrawal sequencing errors are almost never obvious in the moment. Most people draw from whichever account feels most accessible or largest. The tax consequences accumulate gradually — higher effective tax rates, IRMAA surcharges, a growing RMD burden — without any single event signaling that something is wrong.

By the time the pattern becomes visible, restructuring options have narrowed significantly.

Dave maps every withdrawal source — IRA, Roth, taxable, pension, Social Security — across the full retirement timeline before the first dollar is drawn. The sequencing strategy is built around lifetime tax minimization, not convenience or simplicity.

Coordinating withdrawal order with Roth conversion timing and Social Security strategy can meaningfully reduce tax exposure across retirement — but only when the work is done before the pattern becomes fixed.

The Solution

Most financial planning is built around one question: How do I grow my money? The Responsible Retiree Blueprint is built around a different question:

How do I turn what I've built into a life I don't have to worry about?

Before we make a single recommendation, we build a complete picture of your retirement — income, taxes, Social Security, Medicare, investments, and legacy — coordinated together, not managed in silos.

Many people approaching retirement have financial assets spread across multiple institutions — a 401(k) here, an IRA there, a pension from a former employer, a brokerage account opened years ago. Each piece has been managed independently. No one has ever looked at how they work together.

They know they're "probably in good shape." But when asked what retirement actually looks like — monthly income, tax exposure, when to claim Social Security, what Medicare will cost — the picture isn't clear.

The pieces exist. The plan does not.

Fragmented financial relationships are the norm, not the exception. Multiple institutions, a pension administrator, a Social Security timeline that no one has modeled — each advisor manages their piece. No one is looking at the whole picture.

The result is a retirement income plan that hasn't actually been built — just accumulated over time, without coordination, without sequencing, and without a clear picture of what it all produces.

The Blueprint process starts by bringing the full picture into one coordinated plan. Pension income, Social Security timing scenarios, IRA withdrawal sequencing, and IRMAA thresholds are modeled together — not separately.

The goal is straightforward: replace a collection of independent accounts with a single, coordinated retirement income strategy — one that shows exactly what retirement looks like across income, taxes, and time.

The 7 Retirement Dangers

Retirement has landmines that most people never see until they've already stepped on them. We've spent years mapping them so you don't have to learn from experience.

Finding these issues early changes everything. Waiting turns them into expensive regrets that follow you for decades.

Many couples build their retirement picture assuming both spouses will be present throughout. Two Social Security checks. A pension. IRA distributions drawn carefully. On paper, the plan works.

What rarely gets modeled is what happens when the higher-earning spouse dies first. One Social Security check disappears. Pension income may drop significantly. But IRA distributions and Required Minimum Distributions continue — now taxed at single-filer rates that can be nearly double what the couple paid together.

The plan was never built for this. Most aren't.

The widow's tax trap is one of the most predictable and least planned-for challenges in retirement. Household income often drops substantially when one spouse passes, but the surviving spouse's tax bracket frequently increases — because they now file as Single rather than Married Filing Jointly.

The result is a financial picture that looks very different from what either spouse expected. And once it's arrived, the options to restructure are limited.

Dave runs the survivor scenario in every plan — not as a footnote, but as a full analysis. By modeling what income, taxes, and expenses look like for the surviving spouse specifically, the plan can be structured to reduce that exposure before it becomes a crisis.

Roth conversion strategies, withdrawal sequencing, and Social Security timing decisions can all be coordinated with the survivor scenario in mind. The goal is that both spouses leave knowing the surviving partner is genuinely protected — not just assumed to be.

Why Timing Matters More Than You Think

Here is something most people don't realize until it's too late: the best retirement planning moves have expiration dates.

| Roth Conversions | Most powerful in the years before Required Minimum Distributions begin. That window closes — and it doesn't reopen. |

| Social Security Strategy | Requires time to model correctly, stress-test against your income plan, and execute with confidence. |

| Tax Planning | Done before retirement, you have options. Done after the income changes are locked in, you have far fewer. |

| Medicare Cost Control | Premium surcharges are based on income from two years prior. By the time you see them, it's already too late to avoid them. |

| Investment Repositioning | Shifting from a growth-oriented portfolio to a distribution-ready structure takes time — and doing it during a market decline is costly. |

Waiting doesn't just delay your plan. It permanently reduces what your plan can do. The families who retire with the most confidence didn't find a magic investment. They got coordinated earlier, when they still had time to act on what they found.

The best time to build your blueprint was five years ago. The second best time is today.

Many people approaching retirement have the majority of their savings in traditional IRA and 401(k) accounts — pre-tax money that will eventually be taxed as ordinary income. What often isn't visible is that the years just before retirement, when earned income is winding down but Social Security and RMDs haven't started yet, frequently represent the lowest effective tax rates they'll see for the rest of their lives.

That window is one of the most valuable planning opportunities in retirement. Most people move through it without doing anything — not because they made a bad choice, but because no one pointed it out.

The Roth conversion window — the years between today and when RMDs and Social Security fully stack — is narrow and time-limited. Once it closes, the opportunity is gone permanently. Most people miss it because no one is looking at their tax picture holistically across time.

By the time the window becomes visible, it has often already narrowed significantly.

Dave maps the full tax picture across the retirement timeline — identifying when the low-bracket window exists, how wide it is, and how much can be converted each year without triggering IRMAA surcharges or pushing into a higher bracket unnecessarily.

A coordinated Roth conversion strategy, executed before retirement begins, can meaningfully reduce lifetime tax exposure. The opportunity depends entirely on acting while the window is still open — not after the income sources that close it have already arrived.

Who Guides You Through This

Dave Bensch has spent his career working with families navigating the most consequential financial transition of their lives — the years surrounding retirement. Not helping people speculate. Not chasing performance. Building coordinated plans for people who did the work and deserve to retire with confidence.

Dave holds the Certified Financial Planner® designation — one of the most rigorous credentials in the financial planning profession. He is also an IRS Enrolled Agent, which means he doesn't estimate your tax picture. He reads it, with the same depth the IRS demands of its own examiners.

His approach is straightforward: understand your full picture first, identify what's working and what isn't, build a coordinated plan that addresses both — and then execute it with discipline and care. No product quotas. No pressure. Just a plan built around your life.

Learn more about Dave's background and approach →Many people have been with the same financial advisor for years — sometimes more than a decade. They've been told their plan is "on track." The annual reviews happen. The portfolio is discussed.

But certain questions never come up. What does monthly income actually look like in retirement? What happens to the surviving spouse's income and taxes if one partner dies first? How does Social Security timing affect the overall picture? What does the tax situation look like ten or fifteen years out?

Most people don't realize these conversations weren't happening until they finally have one where they are.

Most financial advisors are investment managers first — and retirement income planners rarely at all. The annual review process is built around portfolio performance, not retirement coordination. Clients leave every meeting knowing how their investments performed.

They rarely leave knowing what their retirement actually looks like, what their tax picture is across time, or whether their plan holds if a spouse dies first. The gaps are real, predictable, and largely invisible until someone specifically looks for them.

Dave's first conversations are built around questions that most advisory relationships never ask — about income structure, tax exposure across decades, Social Security timing, survivor protection, and what happens to the plan when markets don't cooperate.

Most people leave that first conversation having discussed their retirement more specifically and honestly than they ever had before. Not because the questions are complicated. Because no one had ever asked them.

Most people arrive at retirement with a savings mindset. Retirement demands a completely different one. This short video explains the shift — and why the families who make it retire with far more confidence than those who don't.

Get Your Retirement Risk Score

You saved for decades. You did the work.

The question now isn't whether you have enough. It's: "Is the plan actually built to deliver what I think it will?"

Most people don't find out the answer until they're already living the retirement. This is where you find out — while there's still time to make it right.

Perrysburg, OH 43551

The most valuable retirement planning decisions — Social Security timing, Roth conversions, withdrawal sequencing — have windows that close. The earlier you act, the more options remain open.

Fourth Dimension Financial Group, LLC ("Fourth Dimension") is an Ohio Registered Investment Adviser. This page is intended for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Actual results will vary. Fourth Dimension does not provide tax or legal advice. Please consult your tax advisor and/or attorney before making decisions with tax or legal implications. Fourth Dimension and its representatives are in compliance with the current registration requirements imposed upon investment advisers by the state of Ohio.