The Journey That Shaped Everything

When Dave Bensch was a college senior, he and his best friend Andrew did something that, looking back, still feels a little crazy. They decided they were going to interview the greatest college basketball coaches in America — Coach K, Dean Smith, Rick Pitino, Tom Izzo, John Wooden. There was just one small problem. They were two broke college kids with no connections, no credentials, and no real plan. All they had was a list of coaches, a lot of nerve, and a Honda Civic.

Somehow, the coaches said yes.

They started making calls, leaving messages, hoping someone would give two college kids fifteen minutes. Five days later they were sitting in Louisville, Kentucky — in Rick Pitino's office. And it just kept working. Over the next fourteen months, they traveled across the country. Coach K at Duke. Tom Izzo at Michigan State. Dean Smith at North Carolina. And in one of the most unforgettable moments, they sat in the living room of John Wooden's home in California. He was in his late nineties. He gave them his time anyway.

It sounds like a basketball story. But it wasn't, really.

What surprised them most was that they didn't talk much about basketball. They talked about leadership, about life, about how these coaches took eighteen-year-old boys and shaped them into men.

Over the course of those conversations, four leadership lessons kept coming up again and again. Lessons that have stayed with Dave ever since — and that still shape how he works with families today.

- Fourteen months. Coaches across the country. Four lessons that kept coming up in every conversation.

- The journey eventually became a book — Destination Basketball — but the real gift was the wisdom those coaches were willing to share.

- Patience. Relationships. Vision. Discipline. The same principles that build championship programs are the ones that build retirement plans that last.

If you enjoy basketball, leadership, or just a good story about two college kids driving across the country in a Honda Civic — Dave would be happy to share a copy of the book with you.

Most financial advisors were trained to manage money. Dave was shaped by something different — by men who had spent their careers turning uncertainty into confidence, and pressure into preparation. That distinction shows up in every conversation he has.

The average advisor walks into a first meeting with a presentation. Dave walks in with questions. The average advisor talks about what the market has done. Dave talks about what your life needs to do. The average advisor manages accounts. Dave builds systems — the same way those coaches built programs. Not for this season. For the long run.

Coach Wooden didn't win ten national championships because he had better players. He won because he built something that held up under pressure, year after year, with whoever was in the room. That's the standard Dave brings to retirement planning. Not a plan that looks good on paper — a plan that holds up across decades, under conditions no one can fully predict.

Our Philosophy

This is not a marketing line. It is the distinction that defines every engagement we take on and every decision we make about how to structure our firm.

The financial services industry has a structural problem: most of the people in it are compensated based on what they sell, not on the quality of the plans they build. That creates a quiet but persistent conflict between what is best for the client and what generates revenue for the advisor. Most clients never see this conflict directly. They just notice, over time, that the recommendations feel a little too convenient.

We built our practice around a different model. We are a fee-based Registered Investment Adviser. We are compensated for the planning we do and the advice we give — not for the products we place. That alignment is not incidental to what we do. It is the foundation of it.

In practice, this means we look at your entire financial landscape before making a single recommendation. Income. Taxes. Social Security. Investments. Medicare. Estate. We look at how every piece interacts with every other piece — across time, across tax scenarios, across market conditions. Because in retirement, nothing happens in isolation. Everything affects everything else.

Structure and coordination are not features we offer. They are the entire point. And because Dave is also an IRS Enrolled Agent, he reads your tax picture — he doesn't estimate it.

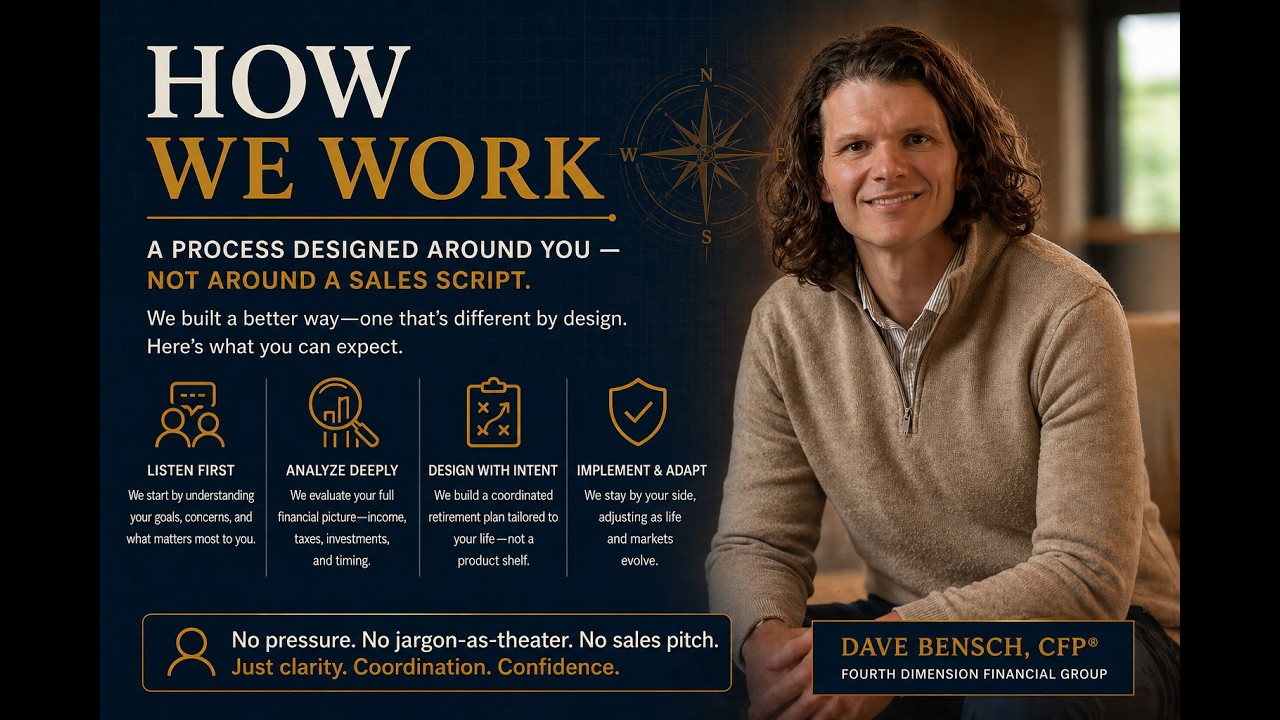

How We Work

We have deliberately built a process that feels unlike any financial advisory experience most people have had. No pressure. No jargon-as-theater. No product presentations dressed up as planning sessions. Just a structured, honest engagement built around one question: what does your retirement actually need to look like, and how do we get you there?

We provide the information. We lay out the options. We tell you what we believe is in your best interest and why. Then you make the decisions — on your own timeline, without pressure. That is the only way this works.

A 61-year-old healthcare executive scheduled what she expected to be a 45-minute product pitch. She had been through these before — polished presentations, impressive-looking charts, and a recommendation that arrived before the advisor had asked a single real question. She had one hand on the door the moment she walked in.

Most financial advisory "first meetings" are structured around the advisor's presentation, not the client's situation. The client spends the hour being educated about the firm's capabilities. They leave with a brochure and a follow-up appointment — rarely with clarity about their own retirement.

Dave spent the first thirty minutes of that meeting asking questions. Goals. Timeline. Concerns about income gaps. Questions about what the surviving spouse situation looked like. By the time he shared anything about the planning process, she already trusted it — because everything he'd said was directly relevant to what she'd just told him.

Who We Serve

We are not the right fit for everyone — and we think it's more respectful to say so upfront than to take every engagement and deliver average results.

We do our best work with people who have worked hard, saved consistently, and built meaningful retirement assets over time. They are thoughtful about money. They are approaching — or recently entering — retirement, and they are beginning to realize that the questions they face now are more complex than anything that got them here.

If that sounds like you — or like someone you're close to becoming — we'd like to have a conversation. Choose the path below that best fits your situation.

Retirement isn't just about having enough. It's about how everything works together — income, taxes, Social Security, timing, survivor protection — in a way that holds across decades you can't fully predict. That understanding is rare. What you do with it is the question.

Schedule Your Strategy Session

The question is no longer "Will I be okay?"

The question is: "Am I unknowingly leaving money, flexibility, or protection on the table?"

Most people don't find out until it's too late to fix. This is where you find out — while the options are still open and the plan can still be built right.

Perrysburg, OH 43551

The coordination windows that matter most — Roth conversions, Social Security timing, withdrawal sequencing — have expiration dates. Every month of delay narrows what's still possible.

Fourth Dimension Financial Group, LLC ("Fourth Dimension") is an Ohio Registered Investment Adviser. This page is intended for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Fourth Dimension does not provide tax or legal advice. Please consult your tax advisor and/or attorney before making decisions with tax or legal implications. Fourth Dimension and its representatives are in compliance with the current registration requirements imposed upon investment advisers by the state of Ohio.